At the beginning of my actuarial career, when I was transitioning from the world of academia, I studied for a part time Master’s degree in Actuarial Finance at Imperial College. As I got to grips with my new industry, a highlight for me was a weekly session where different industry experts would talk to us about their practice areas and pass on wisdom amassed during their careers. The common theme that emerged to me was the importance of actively managing risk. In fact, this seemed so central to actuarial best practice, that I was surprised to learn that “holistic risk management framework integrated into key decision making” was not the motto of the profession.

Following the 2008 economic crisis there has been a growing movement to improve risk management practices underpinning actuarial work, resulting in risk management frameworks being introduced by regulators around the world1 and a growing number of actuaries (particularly those newly qualifying) attaining the global Chartered Enterprise Risk Actuary (CERA) credential2. So maybe the motto change is coming…

Risky business

For defined benefit pension plans, the fact that contributions made today need to cover uncertain promised benefits in the future introduces a number of risks.

Some risks relate to assets – the risks of investing contributions until they are needed. Other risks relate to liabilities – the uncertainty of the level, timing and duration of the benefits that will be paid. There are even risks around how willing and able the sponsor will be to step in if things don’t go according to plan.

Pension plans have embraced the active management of investment risk. The de-risking of assets and a growing adoption of Liability Driven Investment strategies over the last 10 years has resulted in a large reduction of investment risk, leaving liability side risks becoming the largest unhedged funding risks for pension plans in the UK. It is time for liability side risk management to catch up.

Eyes on longevity risk

The key liability risk for a pension plan is longevity risk: the possibility that participants will live longer lives than expected, resulting in the need for more assets to pay benefits. Many pension plans view longevity as an assumption that they need to get ‘right’ rather than recognising it as a risk with a range of potential outcomes that can be measured and actively managed.

Pooling a large number of participants in a pension plan removes risk from random variations of experience between individuals (individual risk) – but this is not the only form of longevity risk. Without robust ways to measure the longevity characteristics of its participants, a plan is exposed to the possibility of systematically mis-estimating the longevity of their participants (basis risk). Even with the best estimation techniques for current longevity, plans are still exposed to the risk that life expectancies change in an unexpected way over time (trend risk). We only need to look at the mortality experience through the recent pandemic for an example of how external events can disrupt previous trends.

Unrewarded does not mean unmanageable

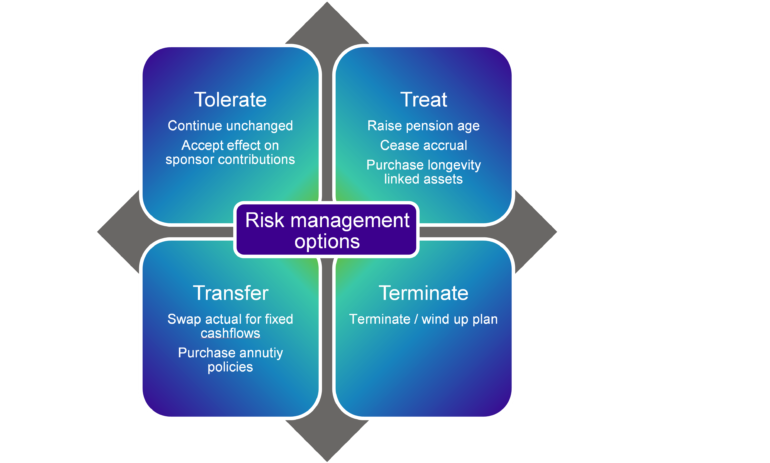

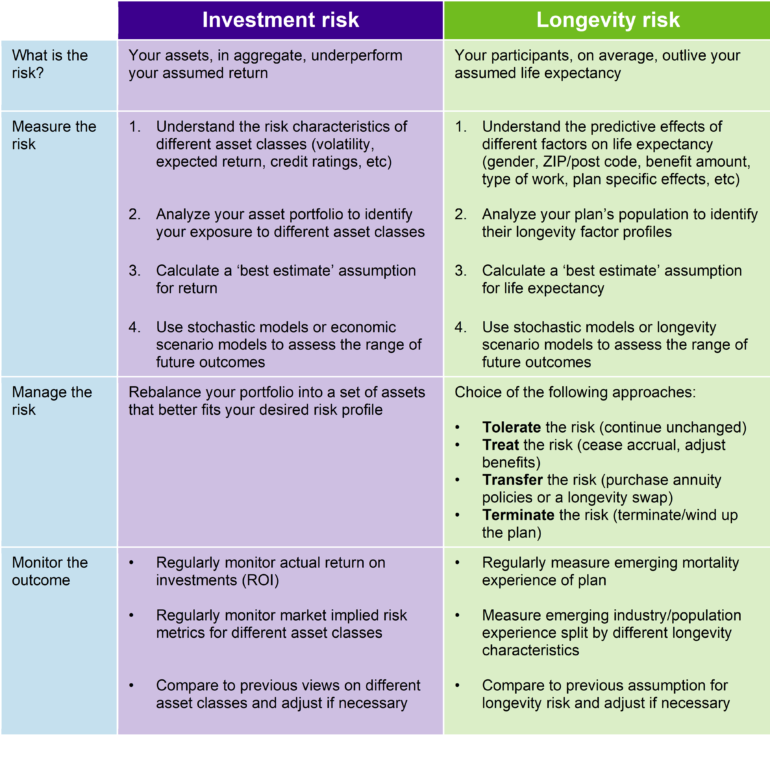

Investment risk is thought of as a ‘rewarded risk’ because investors taking on more risk are compensated with higher expected returns. No such reward exists for pension plans holding longevity risk, but that does not mean that it should be neglected. There are many options for pension plans to manage longevity risk with varying degrees of associated cost.

A new approach?

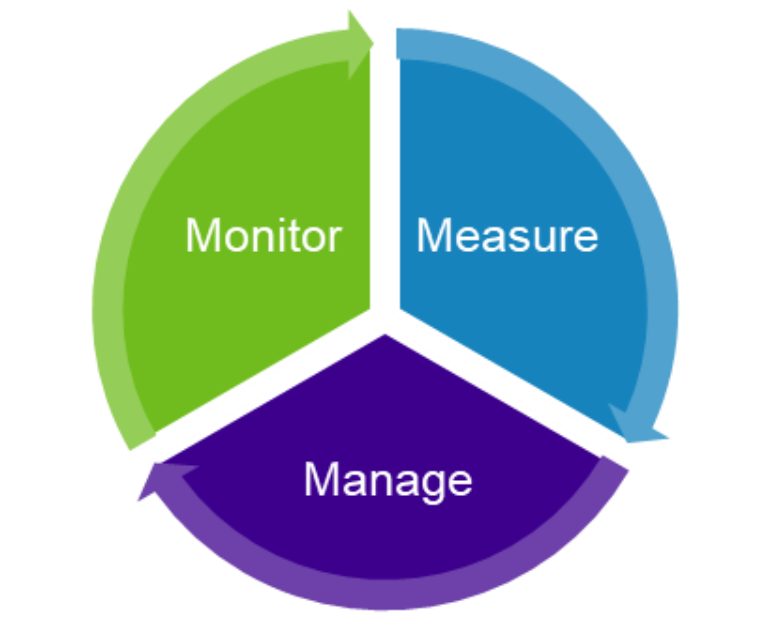

It is difficult to assess the real value of different mitigation options if you don’t have a good grasp of the risk that is being removed. To understand and manage a pension plan’s risks we can apply the actuarial control cycle:

- Measure the risk (define the problem)

- Manage the risk (develop a solution)

- Monitor the outcome

This approach is commonly used by pension plans to manage their investment risk. Below I explore this and the corresponding approach that could be applied to longevity risk.3

What do you think?

How widely do you think longevity risk management techniques are used by pension plans? How long before everyone is using them? How long before the actuarial profession updates its motto?

1 Such as Basel III for the global banking industry, Solvency II for the European insurance industry and the Pensions Regulator’s IRM framework in the UK.

2 Supported by, among others, the Society of Actuaries in the US, the Institute and Faculty of Actuaries in the UK and the Canadian Institute of Actuaries.

3 noting that the ultimate aim is to bring all risks together into one holistic control cycle